Halfway through 2026, the ecommerce M&A market looks nothing like the one founders remember from the cheap-money years. Deal volume has recovered from the 2023 to 2024 trough, but the recovery is uneven and ruthlessly selective. Buyers are active again, capital is available again, and quality assets are trading at numbers that would have looked rich eighteen months ago. Yet weak and unprepared businesses are sitting on the market for months, getting lowballed, or failing to sell at all. The single defining feature of the 2026 ecommerce M&A outlook is the widening gap between what a clean, durable business commands and what an average one can get. This guide breaks down where the market stands at mid-year, how multiples have moved, who is buying, what is driving and stalling deals, and what all of it means if you are thinking about selling in the back half of the year.

This is a market overview for founders of Shopify, DTC, Amazon FBA, and SaaS businesses weighing an exit. It explains the conditions that set your number today rather than the mechanics of any single deal. None of this is financial advice; use it to time your decision and to ask your advisor sharper questions.

Where the Ecommerce M&A Market Stands at Mid-Year 2026

The first half of 2026 confirmed a recovery that began tentatively in late 2025. Transaction activity in online business M&A has climbed back toward the levels last seen before interest rates spiked, and the tone among buyers has shifted from caution to measured confidence. The aggregators that pulled back hard in 2023 have either restructured and returned with cleaner balance sheets or been replaced by more disciplined acquirers. Private equity, strategic operators, and individual buyers are all present, and the bidding for the right asset is genuinely competitive again.

What has not returned is the indiscriminate appetite of the boom. In 2021 a business with growth and a story could attract multiple offers almost regardless of how durable that growth was. In mid-2026 the same business gets careful scrutiny, and buyers underwrite the downside before they discuss the upside. The capital is there, but it is selective capital. It flows to businesses that can prove their earnings and defend their demand, and it walks away from ones that cannot.

The practical result is a two-track market. Prepared, profitable, defensible businesses are clearing quickly and at strong numbers. Everything else is slow. Understanding which track you are on is the most important read a seller can make at mid-year, because the same headline about a recovering market means opportunity for one founder and a long, frustrating process for another.

What defines the mid-year 2026 market:

- Deal volume recovered toward pre-2023 levels, but concentrated in quality assets

- Buyers underwrite downside risk before discussing growth upside

- Capital is available but selective, rewarding proof over narrative

- A widening gap between what clean businesses and average ones command

- Faster closes for prepared sellers, long timelines for unprepared ones

The most common timing mistake: assuming a recovering market lifts every business equally. It does not. The 2026 recovery is a flight to quality, not a rising tide. A founder who reads the headline volume numbers and lists an underprepared business walks into the slow track and learns the hard way that market strength only reaches sellers who have earned it.

For the underlying forces that set the number in any given year, Ecommerce Multiples in 2026 lays out what pushes valuations up and down, and the mid-year picture is those forces playing out in real deals.

How Multiples Have Moved in the First Half of 2026

Multiples are where the two-track market shows up most clearly. At the headline level, average multiples across ecommerce have firmed compared with the 2024 lows, supported by lower financing costs and renewed buyer competition. But the average hides the real story, which is dispersion. The spread between the multiple a top-tier business earns and the one an average business earns has widened to a degree that makes the average almost meaningless as a planning figure.

For healthy DTC and Shopify businesses in the lower middle market, transactions in the first half of 2026 have generally landed in the range of three to just over five times SDE, with the strongest assets, those with diversified traffic, strong repeat revenue, and clean financials, pushing toward and occasionally past the top of that band. Larger businesses with real infrastructure and sustainable EBITDA continue to trade higher, on EBITDA multiples that reflect their lower risk. SaaS has held its premium to ecommerce, with durable recurring-revenue businesses commanding multiples that no physical-product business reaches.

The downward pressure is just as real at the other end. Businesses with concentration risk, declining traffic, thin or undocumented margins, or heavy dependence on a single channel are being discounted hard, and in a selective market that discount often becomes a failure to sell at all. The market is not paying down because money is tight; it is paying down because buyers can afford to be choosy and are pricing risk precisely.

How multiples are behaving at mid-year:

- Average ecommerce multiples firmed off the 2024 lows on cheaper financing

- Healthy DTC and Shopify deals broadly clearing around three to five times SDE

- Top-decile assets pushing past the top of the band on competitive bidding

- SaaS holding a clear premium on the durability of recurring revenue

- Concentrated or declining businesses discounted sharply or stalling entirely

The most common valuation mistake: anchoring on the headline average multiple and assuming your business will earn it. The average is a blend of premium assets and discounted ones, and almost no real business sits exactly on it. A seller who benchmarks against the average instead of against comparable businesses in their own condition sets an expectation the market will not meet.

The factors that decide where in that band a brand lands are the same ones covered in DTC Brand Valuation 2026, and at mid-year they are separating winners from the rest more sharply than ever.

Who Is Buying in 2026

The buyer pool in 2026 is broader and more disciplined than it was at any point in the last three years, and knowing who is at the table changes how a seller should position. Three groups dominate, and each underwrites a deal differently.

Aggregators are back, but they are not the aggregators of 2021. The survivors restructured, wrote down their weaker holdings, and rebuilt around tighter acquisition criteria and healthier financing. They are buying again, particularly in Amazon FBA and consolidatable DTC categories, but they pay for proven profitability and integration fit rather than growth promises. Strategic acquirers, meaning operating companies and brand platforms buying for synergy, have become the most aggressive bidders for the right asset, because they can justify a premium that a financial buyer cannot when the target fills a real gap in their portfolio. Private equity and search funds round out the field, bringing patient capital and a preference for businesses with durable cash flow and a management layer that survives the founder’s exit.

Individual buyers and self-funded operators remain active in the sub-seven-figure range, supported by acquisition financing that has loosened as rates eased. The net effect is that almost every well-prepared business has a natural buyer somewhere in this pool, but the type of buyer most likely to pay a premium depends entirely on the kind of business being sold.

Who is active and what they pay for:

- Aggregators: restructured and disciplined, paying for proven FBA and DTC profitability

- Strategic operators: the most aggressive bidders when the asset fills a portfolio gap

- Private equity and search funds: patient capital favoring durable cash flow

- Individual and self-funded buyers: active in the sub-seven-figure range

- Across all groups: a clear preference for proof of earnings over growth narrative

The most common buyer mistake: marketing to every buyer the same way. An aggregator, a strategic operator, and a private equity fund value completely different things in the same business. A seller who frames their story around what their most likely buyer underwrites, integration fit for a strategic or clean cash flow for a fund, gets a sharper offer than one who sends the same generic pitch to all of them.

The difference in how these buyers think is explored in depth in Aggregators vs Strategic Buyers, and at mid-year 2026 matching your business to the right one is worth real money on the final number.

What Is Driving Deals and What Is Stalling Them

Beneath the volume numbers, a handful of forces are deciding which deals close and which collapse. The tailwinds are real, but so are the headwinds, and the mid-year market is the product of both pulling at once.

On the tailwind side, financing has become cheaper and more available as interest rates eased through late 2025 and into 2026, which directly supports higher multiples because buyers can service more debt against the same cash flow. A backlog of founders who delayed selling during the lean years is now coming to market, adding supply of genuinely good businesses. And dry powder accumulated by funds and aggregators during the slow period needs to be deployed, which keeps competitive pressure on the best assets. These forces explain why quality is clearing fast.

On the headwind side, AI has become the dominant uncertainty in diligence, with buyers marking down businesses whose traffic and demand look exposed to the shift toward AI-mediated buying. Quality of earnings scrutiny has intensified, and deals routinely stall or reprice when a seller’s numbers do not survive verification. Macroeconomic and policy uncertainty, including tariffs and supply chain questions for physical-product businesses, adds caution to any deal with sourcing risk. The result is that good businesses face a fast, competitive process while flawed ones face a slow, skeptical one.

What is moving the market at mid-year:

- Tailwind: cheaper, more available financing lifting what buyers can pay

- Tailwind: a backlog of delayed-sale founders adding quality supply

- Tailwind: accumulated dry powder forcing competitive bidding on top assets

- Headwind: AI exposure marking down traffic-dependent businesses in diligence

- Headwind: intensified quality-of-earnings scrutiny stalling or repricing deals

- Headwind: tariff and supply chain uncertainty adding caution to sourcing-heavy deals

The most common preparation mistake: treating the tailwinds as a reason to rush and ignoring the headwinds that kill deals in diligence. A cheap-financing market gets you offers; clean earnings and defensible demand get you to close. Sellers who ride the tailwind to market without addressing AI exposure and earnings quality are the ones whose deals stall halfway through.

The AI dimension in particular has become its own pricing input, which How AI Is Changing Ecommerce Valuations in 2026 examines in full, and it is now one of the first questions a 2026 buyer asks.

Which Categories Are Hot and Which Are Cooling

The recovery is not spread evenly across categories, and where your business sits shapes both your buyer pool and your multiple. At mid-year 2026, a clear hierarchy has formed between the segments buyers are competing for and the ones they are approaching warily.

SaaS and recurring-revenue businesses remain the most coveted, because durable subscription revenue is exactly the kind of predictable cash flow that survives a five-year hold and an uncertain macro backdrop. Brands with strong owned audiences, meaning real email and SMS lists and high repeat purchase rates, are commanding attention across DTC because that owned demand is what insulates revenue from the AI traffic shift. Consumer health, wellness, and consumable categories with natural replenishment continue to attract premium interest for the same durability reason. On the FBA side, well-run accounts with diversified catalogs and clean account health are trading actively to disciplined aggregators.

Cooling at the other end are businesses built on borrowed attention. Single-channel stores dependent on paid social, content sites monetized through informational search traffic that AI is eroding, trend-driven products without repeat demand, and anything with heavy customer or supplier concentration are all facing thinner buyer interest and wider discounts. The market has not abandoned these categories, but it prices them for the risk they carry, and in a selective environment that often means a long road to a modest exit.

How categories are trading at mid-year:

- Hot: SaaS and recurring-revenue businesses on durability of cash flow

- Hot: DTC brands with strong owned audiences and high repeat rates

- Hot: consumable and replenishment categories with built-in repeat demand

- Hot: clean, diversified FBA accounts with healthy metrics

- Cooling: single-channel and paid-social-dependent stores

- Cooling: content and arbitrage businesses exposed to the AI traffic shift

- Cooling: trend products and anything with heavy concentration risk

The most common positioning mistake: selling into a cooling category without leaning on the durable parts of the business. Even a trend-exposed brand usually has an owned audience or a repeat-purchase core worth foregrounding. A seller who presents the durable revenue first, and frames the rest as upside rather than the foundation, lands in a far better band than one who leads with the volatile topline.

SaaS continuing to hold its premium is no accident, and the mechanics behind it are covered in SaaS Valuation: ARR Multiples Explained, which explains why recurring revenue keeps outpacing physical-product multiples.

What This Means If You Are Planning to Sell in the Second Half of 2026

For a founder weighing an exit in the back half of the year, the mid-year picture points to a clear strategy: the window is genuinely good, but only for sellers who arrive prepared. The recovering market and competitive buyer pool reward the businesses that can prove their case, and they punish the ones that show up hoping the market will carry them. The decision is less about whether to sell into this market and more about whether your business is ready to be sold into it.

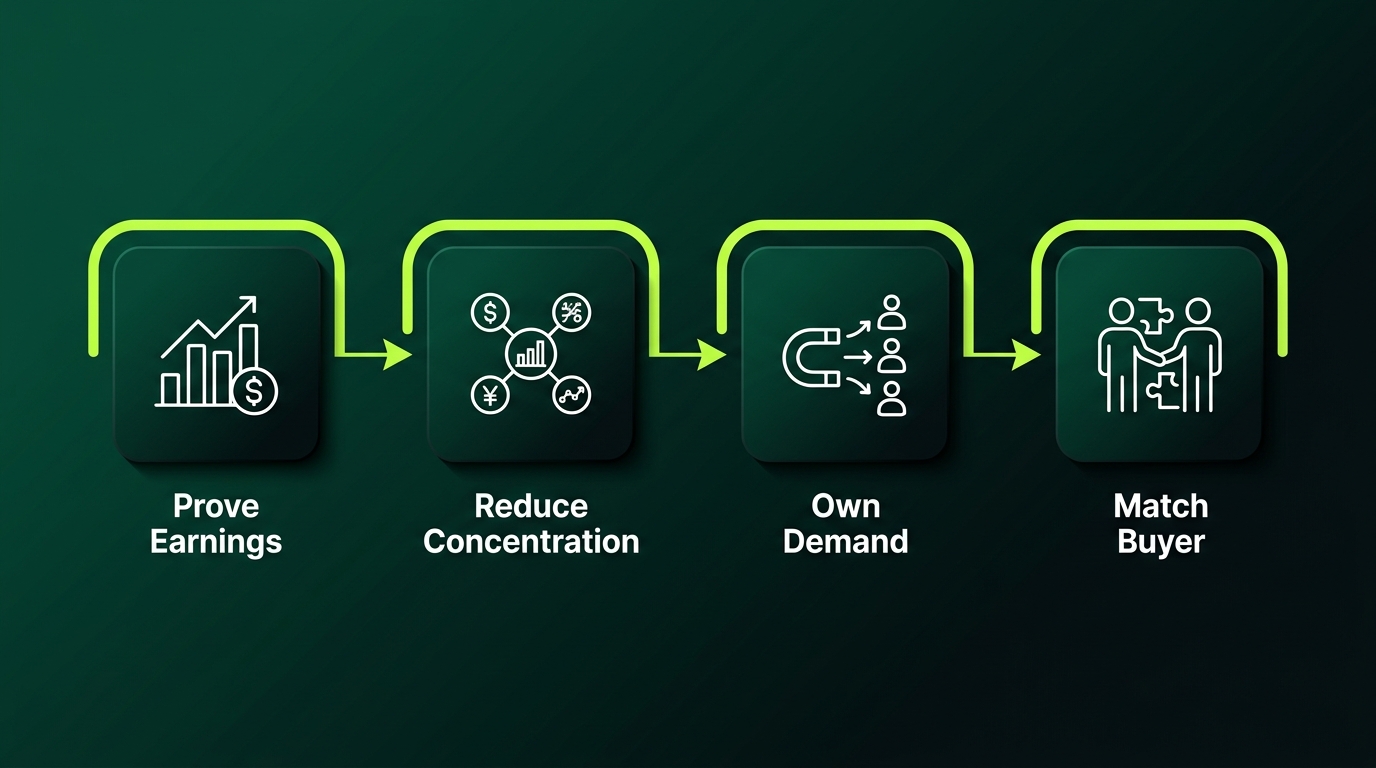

The highest-leverage moves are the ones that move you from the slow track to the fast one. Clean, verifiable financials that survive a quality-of-earnings review are non-negotiable in 2026, because earnings scrutiny is where deals die. Reducing concentration, whether in channels, customers, or suppliers, directly protects your multiple against the risk buyers are pricing most aggressively. Building and documenting owned demand defends you against the AI discount and signals exactly the durability the 2026 buyer is paying for. And matching your story to your most likely buyer, rather than broadcasting a generic pitch, converts interest into competitive offers.

Timing matters too. The tailwinds supporting today’s multiples, easier financing and deployable capital, are favorable but not guaranteed to persist, and the supply of delayed-sale founders coming to market means competition among sellers will build. A prepared business that comes to market in the second half of 2026 meets a strong buyer pool; a business that waits another year to prepare may meet a more crowded field of sellers and a less certain financing backdrop.

What to do before listing in late 2026:

- Get financials clean and verifiable so they survive a quality-of-earnings review

- Reduce channel, customer, and supplier concentration to protect the multiple

- Build and document owned demand to defend against the AI discount

- Identify your most likely buyer type and frame the story around what they value

- Move with intent while financing is favorable rather than waiting for a crowded field

The most common second-half mistake: waiting for a perfect market instead of preparing for a good one. The 2026 window is favorable now, and favorable conditions reward readiness, not patience. A founder who spends the next two quarters getting the business clean and defensible captures this market; one who waits for an even better headline number often finds the window has shifted and the preparation still was not done.

For the full set of moves that lift a number before a sale, DTC Brand Valuation 2026 details the factors buyers reward, and getting them right is what separates a fast 2026 close from a stalled one.

Bottom Line

The 2026 ecommerce M&A market has recovered, but it has recovered as a flight to quality rather than a return to the boom. Deal volume is up, financing is cheaper, and the buyer pool of aggregators, strategics, and funds is competitive again, yet all of that strength flows to businesses that can prove their earnings and defend their demand. The gap between what a clean, durable business commands and what an average one can get has never been wider, and that gap is the defining feature of the mid-year outlook.

For sellers, the message is that this is a good market to exit into, provided you arrive on the fast track. Clean financials, low concentration, owned demand, and a story matched to the right buyer are what move a business from the slow, skeptical process to the fast, competitive one. The headwinds, AI exposure and intensified earnings scrutiny, are exactly the things preparation neutralizes.

If you are considering a second-half exit, the work to do is clear and the window is open. Start by understanding how the market sets your number in Ecommerce Multiples in 2026, then build the durability case with DTC Brand Valuation 2026. The founders who prepare now meet this market at its best; the ones who wait risk meeting a more crowded one later.