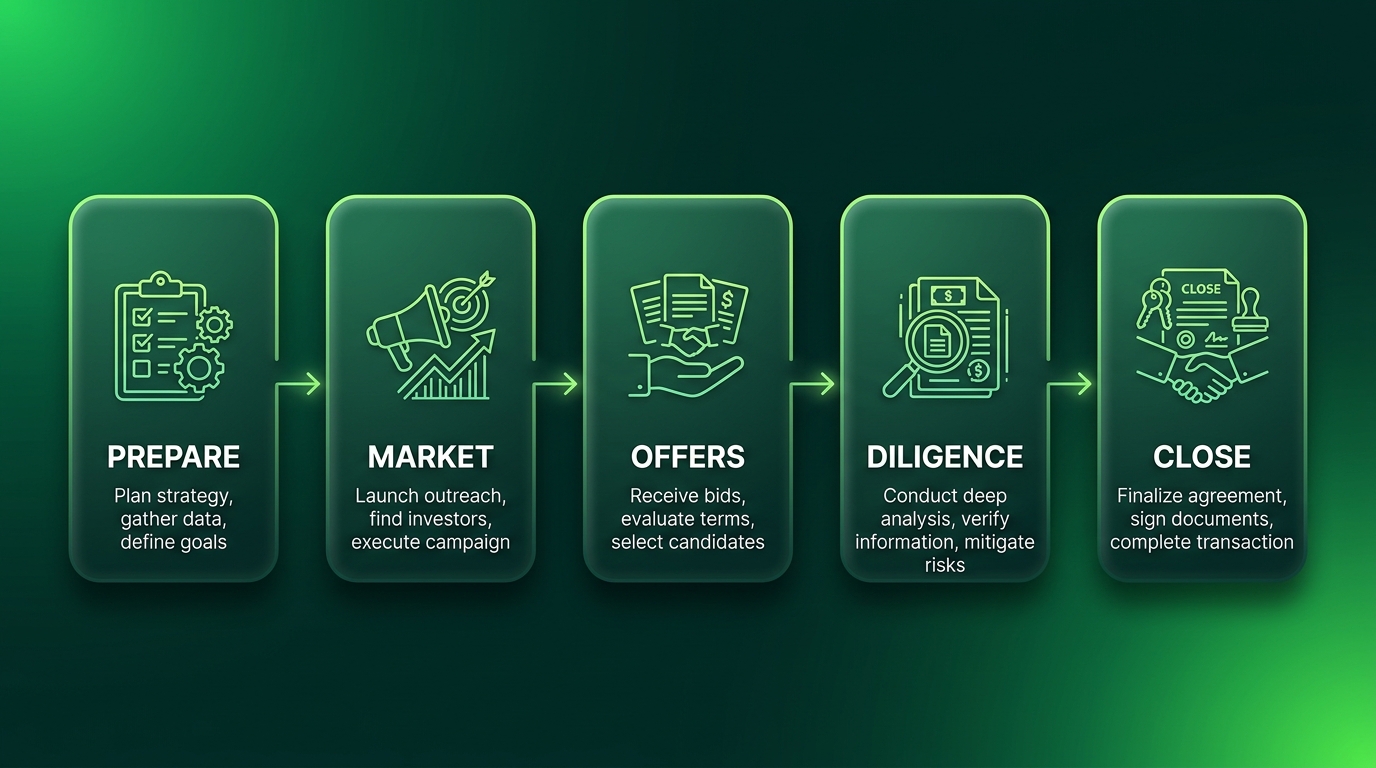

The buyer you choose changes the deal more than the multiple you negotiate. Two offers at the same headline price can produce wildly different outcomes for the founder, because an aggregator, a strategic acquirer, and a private equity firm each value your business for different reasons, pay in different structures, and treat what you built in completely different ways after closing. The founders who exit best do not just chase the highest number. They understand which type of buyer they are actually talking to and what that buyer really wants.

This guide breaks down the main categories of ecommerce buyers in 2026, what each one looks for, how their offers tend to be structured, and how to decide which fits your business and your goals. The aggregator landscape in particular has changed sharply since the 2021 boom, and reading that shift correctly matters. None of this is financial advice; use it to ask sharper questions of the buyers across the table.

The Buyer Landscape Has Changed Since 2021

For a few years, the ecommerce exit market had one dominant story: aggregators. Funded by enormous rounds of capital, roll-up companies like the best-known FBA aggregators competed aggressively to buy Amazon businesses, often at premium multiples and with fast, standardized processes. For a seller in 2021, the aggregator was frequently the obvious buyer.

That environment is gone, and pretending otherwise leads to bad decisions. Higher interest rates, the end of cheap capital, and the operational reality that running dozens of acquired brands is genuinely hard reshaped the category. Some aggregators consolidated, some restructured, and some exited buying entirely. The survivors are more disciplined, more selective, and far more focused on quality of earnings than on growth at any cost.

At the same time, other buyer types have stepped forward. Strategic acquirers, established companies buying brands that fit their portfolio, have become more active, especially for brands with real differentiation. Private equity and search funds look for businesses with durable cash flow. And individual operators, often first-time buyers using acquisition financing, remain a steady source of demand for smaller deals.

What changed in the buyer market:

- Aggregators are fewer, more selective, and focused on clean, profitable, well-documented businesses

- Strategic buyers have grown more active, paying for fit and synergy rather than just financials

- Private equity and search funds prioritize durable, transferable cash flow over rapid growth

- Individual operator-buyers remain strong demand for businesses under roughly one to three million dollars

- Across all types, quality of earnings and clean books matter more than they did in the boom

The most common buyer-market mistake in 2026: anchoring expectations to 2021 aggregator multiples. The premium, no-questions environment is over. Sellers who price and posture as if it still exists stall their processes and signal that they have not done their homework.

Understanding who is actually buying is the first step to reaching them. How to Find Qualified Buyers for Your DTC Brand covers how to source and screen across these categories rather than betting on a single buyer type.

What an Aggregator Actually Wants

An aggregator is a company whose business model is buying, operating, and growing a portfolio of ecommerce brands, most often Amazon FBA businesses. They are financial operators at heart: their thesis is that they can run your brand more efficiently at scale, applying shared supply chain, advertising, and operational expertise across many businesses at once.

Because of that model, aggregators value predictability and transferability above almost everything else. They want a business that runs on systems rather than on the founder, with clean financials, stable rankings, and defensible products. A brand whose success depends heavily on the founder’s personal content, relationships, or constant intervention is harder for an aggregator to absorb, because their whole advantage comes from plugging a business into a standardized operating machine.

Aggregator offers tend to follow recognizable patterns. They often include a meaningful upfront cash component plus structured payments such as earnouts or holdbacks tied to post-sale performance. They move relatively quickly and have repeatable diligence processes, since buying businesses is what they do all day. But in 2026 they are disciplined on price and quick to walk from messy financials.

What aggregators look for:

- Stable, transferable operations that do not depend on the founder day to day

- Clean, well-documented financials that survive a quality-of-earnings review

- Defensible products with consistent rankings and reviews, ideally with some moat

- A product line that fits efficiently into their existing supply chain and ad infrastructure

- Realistic seller expectations on price and deal structure

The most common mistake with aggregators: assuming the headline number is the takeaway value. Aggregator offers frequently load a portion of the price into earnouts and holdbacks contingent on future performance. Read the structure, not just the total, and understand exactly what you must do to actually receive the back end.

If your business is an Amazon-centric brand, the mechanics of selling to this category are covered in How to Sell an Amazon FBA Business in 2026, which goes deeper on the FBA-specific diligence aggregators run.

What a Strategic Buyer Actually Wants

A strategic buyer is fundamentally different. This is an established company, often in your category or an adjacent one, that wants your brand because it advances their own business. They are not buying a financial asset to optimize; they are buying a capability, a customer base, a product line, or a market position they would otherwise have to build themselves.

That difference changes everything about how they value you. A strategic buyer can often justify a higher price than a purely financial buyer because they capture synergies a financial buyer cannot: cross-selling your products to their customers, putting your brand into their retail distribution, folding your products into their manufacturing, or simply removing a competitor. They are paying for what your business is worth inside their company, which can exceed what it is worth on its own.

Strategic deals also tend to look different in practice. They can be slower and more relationship-driven, since a corporate development team and multiple stakeholders are involved. The founder’s role afterward varies widely: some strategics want the founder to stay and lead, others fold the brand in and move on. And because the rationale is strategic, the fit between the two businesses matters as much as the financials.

What strategic buyers look for:

- A brand or product that fills a specific gap in their portfolio or roadmap

- Customer relationships, audience, or distribution they want to acquire rather than build

- Differentiation and brand equity that would be expensive to replicate

- Synergy potential, whether in revenue, supply chain, or market position

- Cultural and operational fit, since they intend to integrate the business

The most common mistake with strategic buyers: leading with financials when you should be leading with fit. A strategic pays a premium for what your business does for theirs. If your pitch reads like a spreadsheet rather than a strategic rationale, you leave the synergy premium, the very reason they pay more, on the table.

The clearest illustration of strategic value is a real deal. Inside Marzetti’s $400M Bachan’s Acquisition: A Strategic Exit Breakdown shows how a strategic acquirer paid for distribution and category position, not just earnings, and what that meant for the founders.

Private Equity, Search Funds, and Individual Operators

Aggregators and strategics get the headlines, but a large share of ecommerce deals close with three other buyer types, and each suits a different kind of business and founder. Knowing where you fit prevents you from forcing a conversation with the wrong category.

Private equity firms buy for durable cash flow and a future resale. They want businesses stable and large enough to support professional management and, often, debt. For most PE firms, that means a floor on size, frequently a million dollars or more in profit, and a strong preference for diversified, defensible revenue. They may keep the founder on, install their own operators, or use the business as a platform to acquire more. The upside for a seller is a credible, well-funded buyer; the trade-off is a rigorous, sometimes slow process.

Search funds and individual operator-buyers occupy the other end. A searcher is typically an entrepreneur who has raised capital specifically to buy and run one business. An individual buyer is often self-funded or using acquisition financing. Both tend to focus on smaller businesses, both value a smooth transition heavily, and both care deeply about whether they can actually run the business after you leave. For founders of sub-million-dollar businesses, these buyers are frequently the most realistic and motivated audience.

What distinguishes these buyers:

- Private equity wants durable cash flow, scale, and a path to a future exit, usually with a size floor

- Search funds want a single solid business they can operate, with strong seller transition support

- Individual operators want a business they can personally run, often financed, usually smaller

- All three weigh transferability and owner dependence heavily, since they must run it without you

- Process rigor scales with the buyer: PE is most formal, individual buyers least

The most common mistake across these buyers: ignoring owner dependence. Financial and individual buyers are buying a business they must operate without you. If too much of the value lives in your head, your relationships, or your personal brand, every one of these buyers discounts the price or walks. Document and delegate before you go to market.

Matching the Buyer to Your Business and Your Goals

There is no universally best buyer. The right one depends on what your business is and what you actually want out of the exit, and those two questions deserve honest answers before you talk to anyone. A founder optimizing for the cleanest, fastest exit has different priorities than one optimizing for the absolute highest price or for the brand’s future.

Start with the business itself. An Amazon-heavy brand with systematized operations and clean books is squarely in aggregator and operator territory. A differentiated DTC brand with real equity, a loyal audience, or unique distribution is where strategics can pay the most. A larger, diversified business with durable profit is what private equity is built for. A smaller owner-operated store is the natural home of searchers and individual buyers.

Then weigh your own goals, because they change which offer is genuinely best. If you want to be fully out quickly, a buyer that loads the deal with multi-year earnouts is a poor fit regardless of headline price. If you care about the brand’s legacy and your team, a strategic with a clear integration plan may beat a financial buyer who will strip costs. If maximizing price is the only goal, you want competitive tension across multiple buyer types, not a single bidder.

What to weigh when matching buyer to business:

- Business profile: Amazon-centric versus differentiated DTC versus large and diversified versus small owner-run

- Your timeline: how quickly you want to be fully out, and your tolerance for earnouts

- Your priorities: top price, clean exit, team and brand legacy, or speed and certainty

- Deal structure tolerance: how much contingent or deferred payment you will accept

- Post-sale role: whether you want to stay involved, and in what capacity

The most common matching mistake: running a process for one buyer type and accepting their framing of value. The way to maximize both price and fit is competitive tension. Multiple buyer types bidding against each other not only raises the number, it reveals which buyer truly values what you built.

Different buyers also justify different multiples, which is why the same business can be worth different amounts to different acquirers. Ecommerce Multiples in 2026 breaks down how the multiple actually gets set and why a strategic premium is real but not guaranteed.

How Each Buyer Runs Diligence and Closing

The buyer type shapes not just the price but the entire experience of selling, especially diligence and the transition. Knowing what to expect lets you prepare for the specific process you will face rather than a generic one.

Aggregators and private equity run the most systematic diligence. Expect a thorough quality-of-earnings review, detailed scrutiny of your financials, and probing on transferability and risk. These buyers do this repeatedly and have checklists; clean, organized records move their process fast, while messy books stall or kill it. Strategics add a layer of strategic and integration review on top, evaluating not just whether the numbers are real but whether the business fits theirs. Individual buyers and searchers run lighter but more anxious diligence, because the decision is personal and they often have less margin for error.

The transition differs just as much. Aggregators plug the business into their machine and usually want a defined, time-boxed handover. Strategics may want a longer, deeper involvement if they value your leadership, or a clean integration if they do not. Financial buyers want enough transition to de-risk operations. Individual buyers usually want the most hands-on training, since they are about to run the business personally.

What to prepare for, by buyer:

- Aggregators and PE: rigorous quality-of-earnings and financial diligence, time-boxed transition

- Strategics: strategic and integration review on top of financials, variable founder role

- Individual buyers and searchers: lighter but more cautious diligence, heavy training needs

- All buyers: clean, organized records that survive scrutiny without surprises

- Every type: a clear, documented transition plan that reduces their perceived risk

The most common closing-stage mistake: underestimating how much diligence intensity varies by buyer and arriving unprepared for the one you get. The fix is universal: organized financials, documented operations, and a clear transition plan reassure every buyer type and protect your price when scrutiny peaks.

Bottom Line

The choice between an aggregator, a strategic, a financial buyer, and an individual operator is not a detail of the deal. It is the deal. Each values your business for a different reason, structures offers differently, and treats what you built differently after closing, and the 2026 market rewards founders who understand those differences rather than chasing a single buyer type out of habit.

The aggregator-at-any-price era is over, which is not bad news; it just means the market is more rational. Aggregators still buy clean, transferable, profitable businesses. Strategics pay premiums for fit and synergy. Private equity and operators provide steady, credible demand for the right profiles. The winning move is to know which category your business actually fits, get honest about your own goals, and then create competitive tension so the buyer who values you most has to prove it with their offer.

Do that, and the right buyer is not a matter of luck. It is the predictable result of a well-run process. Start by understanding who is actually in the market and how to reach them in How to Find Qualified Buyers for Your DTC Brand, then pressure-test your number against Ecommerce Multiples in 2026.