Most ecommerce founders spend months preparing their financials, cleaning up their Shopify backend, and assembling a data room before going to market. Many of them delay hiring a lawyer until they have a signed letter of intent in hand. That delay is one of the most common and costly mistakes in the entire sale process.

A transaction attorney is not just someone who reviews documents at the finish line. The right lawyer shapes how your deal is structured, protects your interests during negotiation, identifies risks you would not have spotted yourself, and ensures that what you sign actually reflects what you agreed to. An attorney retained early can change the outcome of your deal in ways that far exceed their fee.

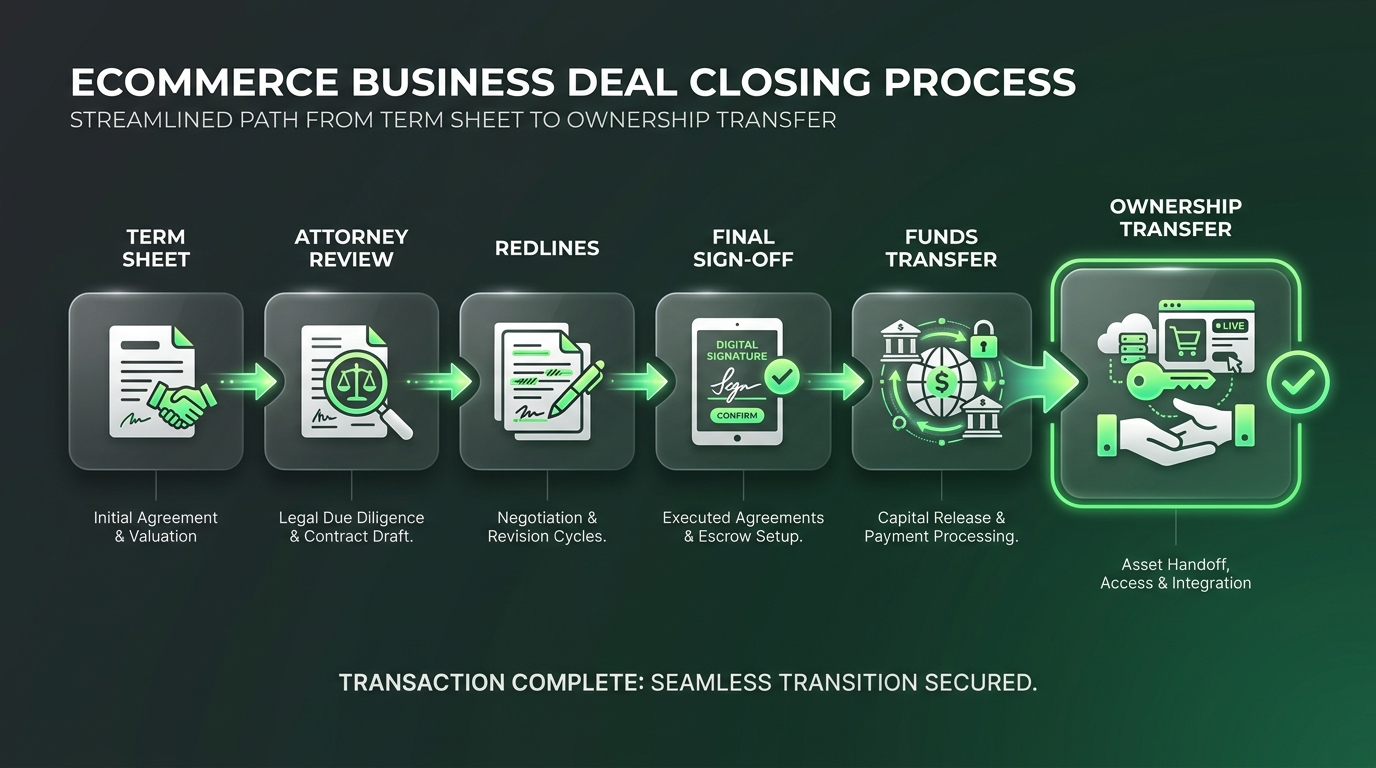

This guide covers when to hire a lawyer, what kind of specialist you need, how to vet candidates, what the legal scope looks like across a full ecommerce sale, and how much you should expect to pay. For the deal structure context that informs most of this, start with Asset Sale vs. Stock Sale for Ecommerce Exits and Letter of Intent (LOI) Guide for Ecommerce Sellers before continuing here.

Why Most Sellers Underestimate Legal Costs and Scope

Founders who have never sold a business before consistently underestimate two things: how long legal review takes and how many decisions are actually legal decisions. Pricing your business, choosing a buyer, and negotiating your multiple feel like business decisions. But the moment you sign an LOI, almost everything becomes a legal matter.

The Asset Purchase Agreement (APA) or Stock Purchase Agreement (SPA) that governs your deal will determine what assets actually transfer, which liabilities stay with you, how representations and warranties are structured, what happens if something goes wrong after closing, and dozens of other provisions that can affect the economics of your deal for years after the wire clears.

Sellers who try to minimize legal spend by using a general-purpose attorney, reviewing documents themselves, or relying on the broker to handle legal matters make these assumptions:

- That the buyer’s attorney is neutral or will catch issues that protect both parties

- That standard boilerplate is fine for their specific deal structure

- That they understand the indemnification and representations clauses well enough to evaluate risk

- That escrow holdbacks, working capital adjustments, and earnout mechanics are straightforward

None of these assumptions are safe. The buyer’s attorney represents the buyer. Standard templates are drafted to favor the party with more leverage. Indemnification clauses regularly expose sellers to post-close liability that erases meaningful percentages of deal value. A qualified M&A attorney pays for themselves on these issues alone.

The most common legal mistake: signing an LOI before legal counsel reviews it. Most LOIs include exclusivity periods, no-shop clauses, and initial representations that set the tone for the entire deal negotiation. Once signed, these terms are difficult to unwind. Have an attorney review the LOI before you sign, not after.

What Kind of Attorney You Actually Need

Not all lawyers are qualified to handle an ecommerce M&A transaction. This is a specialized area that requires familiarity with digital asset transfers, platform-specific account transition requirements, IP assignment, SDE-based deal structures, and the mechanics of earnouts and seller notes common in the sub-$10M ecommerce deal market.

The three categories of attorney you might consider for an ecommerce sale are:

M&A Transaction Attorney

This is what you want. An attorney whose practice focuses on mergers and acquisitions, business sales, and deal structuring. Ideally, someone who has worked on at least a dozen small-to-mid-market deals and understands the specific mechanics of Shopify, Amazon FBA, and DTC brand transactions. They will draft and negotiate your APA or SPA, review reps and warranties, structure the escrow, and handle closing documents.

Business Attorney (General Practice)

A generalist business attorney can handle some aspects of your transaction, particularly if your deal is simple and below $1M in value. They can review an NDA, a basic LOI, and assist with entity-level documentation. What they typically cannot do well: negotiate complex M&A-specific language, structure earnout provisions, or advise you on deal structures they have not personally executed before.

IP or Domain Attorney (Supplemental)

For brands with registered trademarks, patents, or complex IP portfolios, you may need a dedicated IP attorney to handle the assignment and transfer of those assets. This is usually a supplemental engagement alongside your primary M&A attorney, not a replacement for one. Your M&A attorney should be able to refer you to qualified IP counsel if needed.

The single most common attorney mismatch: hiring a real estate attorney or a general corporate attorney because they helped you set up your LLC three years ago. M&A transactions have specific mechanics that generalists rarely encounter. A well-meaning but inexperienced attorney can miss critical provisions or fail to negotiate terms that a specialist would have addressed immediately.

When to Engage Legal Counsel in the Sale Process

The ideal time to engage a transaction attorney is before you go to market, not after you receive an offer. At minimum, you want legal counsel in place and briefed before you sign any binding document. Here is how legal involvement maps to the typical ecommerce sale timeline:

Pre-Market (6 to 12 Months Out)

If you are preparing your business for sale over a longer horizon, an attorney can review your existing contracts, supplier agreements, and IP registrations for issues that would surface in diligence. Catching a problem 12 months before your target close is very different from catching it 30 days into a review period with a buyer waiting.

What to document and prepare during this phase:

- Review all supplier and vendor contracts for assignability clauses

- Confirm trademark registrations are current and in the business’s name

- Ensure domain registrations and social media accounts are in business entities, not personal accounts

- Review any existing non-compete or non-solicitation agreements that could bind you post-sale

- Confirm there are no pending disputes, claims, or IP issues that would need disclosure

LOI Stage (Before Signing)

This is the most critical moment for legal review. An LOI may feel informal, but it sets binding terms: exclusivity period length, no-shop clause, confidentiality obligations, and often preliminary representations about deal price and structure. Many sellers treat the LOI as a handshake document. It is not.

What your attorney should review in the LOI:

- Length and terms of the exclusivity period (standard is 30 to 60 days; longer exclusivity means more risk if the deal falls apart)

- No-shop clause scope and what it prevents you from doing during exclusivity

- Any binding representations or warranties already embedded in the LOI

- Working capital targets or adjustments referenced in the LOI

- Deposit or good-faith payment terms and refund conditions

- Deal structure indicated (asset vs. stock) and whether it accurately reflects what was discussed

Due Diligence and Negotiation

During the review period, your attorney is not passive. They are reviewing documents the buyer requests, advising on what to disclose and how to frame it, and beginning to negotiate the draft purchase agreement in parallel with the document exchange. This is where the real legal work happens.

Purchase Agreement and Closing

The APA or SPA is the governing document for the entire transaction. Every significant term of your deal, including price adjustments, earnout mechanics, indemnification caps, rep and warranty survival periods, and the scope of assets transferred, is defined here. Your attorney negotiates this document line by line with the buyer’s counsel. This phase typically takes two to four weeks for a well-prepared deal.

How to Evaluate and Select an M&A Attorney

Finding the right attorney for your ecommerce sale is not as simple as searching for an M&A lawyer in your city. The market for sub-$10M ecommerce deals is specific, and not every transactional attorney understands the mechanics of digital asset transfers, platform account transitions, or the SDE-based valuation framework that governs most deals in this range.

What to evaluate when selecting legal counsel:

- Deal volume in your size range: Ask specifically how many deals they have closed in the $500K to $10M purchase price range in the last 24 months. This is your market. Experience on $50M corporate deals does not translate directly.

- Ecommerce and digital asset familiarity: They should understand Shopify account transfers, Amazon Seller Central transfers, IP assignment for digital brands, and the mechanics of an SDE-based deal. If they are unfamiliar with these terms, they are not the right fit.

- Responsiveness and bandwidth: M&A deals move quickly. An attorney who takes 72 hours to return calls during a negotiation window is a liability. Ask about their typical response time and current deal load.

- Fixed fee or hourly rate clarity: Understand the billing structure before engaging. Some attorneys offer flat fees for standard transactions. Others bill hourly. Get an estimate range and ask what typically drives deals above estimate.

- References from comparable deals: Ask for references from sellers who closed deals in a similar size range in the last 12 months. A qualified attorney should be able to provide these without hesitation.

What to ask in your first call: How many ecommerce asset sales have you personally closed in the last 12 months? Have you worked on Shopify or Amazon account transfers specifically? What does your typical fee look like for a deal in the $2M to $5M range? A strong M&A attorney will have direct answers. Vague responses are a signal to keep looking.

Where to find qualified candidates: your broker is often the best first referral source. Brokers who work on ecommerce deals regularly have relationships with attorneys they trust to move efficiently and not overcomplicate transactions. Your accountant and other founders who have sold businesses in your size range are also strong sources. Cold outreach to law firm websites is the least reliable approach.

What Legal Fees Actually Look Like

Legal fees for an ecommerce sale vary significantly based on deal complexity, deal size, and whether the transaction involves any unusual issues (contested IP, complex earnout structures, multi-entity businesses, or litigation disclosure). Below is what sellers should expect at different deal tiers in the current market.

Sub-$1M Purchase Price

In this range, many deals use simplified documentation and lighter legal processes. A qualified attorney can often review and negotiate the full transaction for $3,000 to $7,000 in total fees. If the deal is a pure asset purchase with straightforward documentation, some sellers in this range use a flat-fee arrangement with a junior M&A attorney or a specialized online business transaction service.

$1M to $5M Purchase Price

This is where most ecommerce deals land, and where legal fees start to reflect real complexity. Expect total legal fees in the range of $8,000 to $20,000 for a reasonably clean deal. Deals with earnout provisions, working capital adjustments, seller notes, or multiple entities on either side of the transaction will trend toward the higher end of that range.

$5M to $15M Purchase Price

At this size, deals typically involve institutional or strategic buyers, more rigorous due diligence, and significantly more complex purchase agreements. Legal fees commonly run $20,000 to $50,000 or more. Reps and warranties insurance is increasingly common at this tier, which adds an insurance placement process alongside the legal work.

One fee item that surprises many first-time sellers: escrow and closing costs. These are separate from attorney fees and typically run 0.1% to 0.25% of the deal value, paid to the escrow service that holds and releases funds at closing. Your attorney will coordinate this process, but it is a separate line item.

For the tax implications that structure choices create, including how asset vs. stock election affects your post-close tax liability, see our companion guide on the tax implications of selling your ecommerce business.

Key Legal Documents You Will Sign

Understanding what you are signing at each stage is part of working effectively with your attorney. You are not expected to negotiate these documents independently, but you should understand what each one covers before you review it with counsel.

Non-Disclosure Agreement (NDA)

The first document in any serious sale process. An NDA restricts the buyer from sharing your financial and operational information with third parties and from using that information if the deal does not proceed. NDAs in ecommerce transactions are largely standard, but your attorney should review any NDA that includes unusual carve-outs or survival periods shorter than two years.

Letter of Intent (LOI)

The LOI outlines the proposed deal terms before a full purchase agreement is drafted. It is typically non-binding on price and structure but binding on exclusivity and confidentiality. As noted in the LOI Guide for Ecommerce Sellers, the LOI is where deal terms are first established in writing. Changes made after LOI signing are harder and more expensive to negotiate.

Asset Purchase Agreement (APA) or Stock Purchase Agreement (SPA)

The governing transaction document. For most ecommerce deals, this will be an APA rather than an SPA, because buyers prefer asset purchases in this market. The distinction matters significantly for tax treatment and liability allocation. See Asset Sale vs. Stock Sale for Ecommerce Exits for a full breakdown of how these two structures compare.

Transition Services Agreement (TSA)

Common in ecommerce deals, the TSA defines what the seller agrees to do after closing to support the transition. This includes things like staying available for questions, facilitating platform account transfers, introducing the buyer to key suppliers, and providing hands-on training for operational handoff. TSA duration is typically 30 to 90 days and is often compensated separately from the purchase price.

Non-Compete Agreement

Most buyers require the seller to sign a non-compete agreement restricting them from starting a competing business for a defined period (typically two to four years) within a defined scope (the same product category and market). Non-competes are negotiable. The scope, duration, and carve-outs for consulting activity are all standard negotiation points. Your attorney should review these provisions carefully, because overly broad non-competes can restrict your professional activity well beyond what is reasonable.

Red Flags to Watch For in Legal Representations and Warranties

Representations and warranties (reps and warranties) are the section of your purchase agreement where you make formal statements about the business that the buyer is relying on. If those statements turn out to be inaccurate after closing, you can be held liable for indemnification. Understanding the reps you are making and where your exposure lies is one of the most important jobs your attorney does.

Issues to review carefully with your attorney:

- Indemnification cap and basket: The cap limits how much you can be held liable for post-close indemnification claims. The basket (or deductible) is the threshold below which claims cannot be made. These are negotiable and significantly affect your post-close risk.

- Survival period: Reps and warranties survive closing for a defined period, typically 12 to 24 months for general reps and longer for fundamental reps (title, authority, IP ownership). Know what survives and for how long.

- Bring-down conditions: The buyer will require you to certify at closing that all reps remain true as of the closing date. If anything material has changed between signing and closing, you must disclose it. Failing to do so creates post-close liability.

- Supplier contract representations: If you have represented that all supplier contracts are in good standing and assignable, and one turns out not to be, that is a breach of rep. Confirm every supplier agreement before signing.

- IP ownership representations: You will represent that you own all IP being transferred free and clear of claims. If any branding, product design, or content was created by a third party without a proper work-for-hire agreement, this is a gap that needs to be resolved before closing.

The most common post-close indemnification claim: undisclosed or inaccurate revenue and financial representations. Buyers who discover that stated revenue figures were inaccurate, or that significant addbacks were unsupported, will pursue indemnification claims. Your attorney’s review of the financial reps section is a direct risk management function, not a formality.

Bottom Line

Hiring a qualified M&A attorney is not a legal formality at the end of your ecommerce sale. It is a strategic decision that affects how your deal is structured, what you sign, how much risk you carry after closing, and whether the economics of the transaction you agreed to in principle actually hold up in the final documents.

The right attorney pays for themselves many times over: through negotiated indemnification caps that limit your post-close exposure, through representations reviewed carefully enough to prevent future claims, through a non-compete scoped narrowly enough to preserve your professional options, and through a closing process that moves quickly because the documents are handled correctly the first time.

Engage legal counsel before you go to market if you can. At minimum, engage before you sign an LOI. The cost of waiting until the purchase agreement stage is higher than the cost of the attorney.

For the full process picture, see Working With an Ecommerce Broker: What to Expect. For the deal structure decisions your attorney will need to advise on from day one, review Asset Sale vs. Stock Sale for Ecommerce Exits.

If you are preparing your ecommerce business for sale and want to know what it is worth before you bring in counsel, EcomSwap offers free valuations for qualified DTC, Shopify, and Amazon FBA businesses. Our team works with founders at every stage of exit preparation, from early-stage clean-up to active listing and deal negotiation.