A SaaS business generating $500,000 in annual recurring revenue will typically sell for $2 million to $4 million. A DTC brand generating $500,000 in seller’s discretionary earnings will typically sell for $1.25 million to $2.5 million. Same revenue figure, different structure, and a meaningful gap in exit value. That gap is not a flaw in how ecommerce businesses are valued. It reflects real differences in revenue predictability, margin profiles, and operational risk that buyers price in across both asset classes.

If you are a DTC or Shopify founder who has read about SaaS multiples and wondered whether you are leaving money on the table, this guide explains exactly how SaaS and ecommerce multiples are calculated, why they differ, and what ecommerce sellers can do to close the gap before going to market.

How SaaS Multiples Work

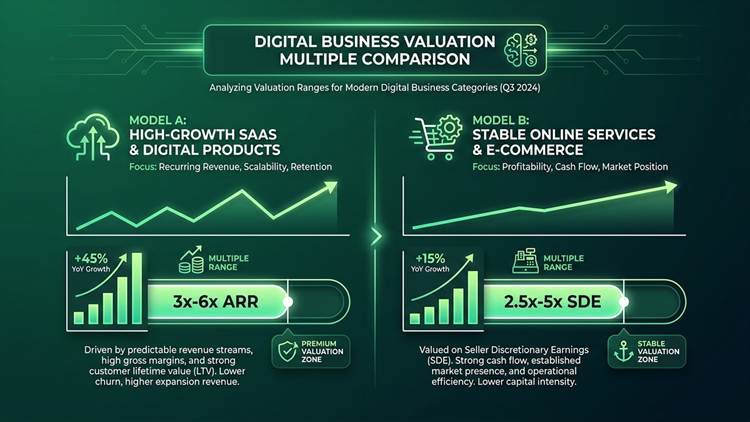

SaaS businesses are valued primarily on a revenue multiple applied to annual recurring revenue (ARR). The most common framework uses ARR as the base because recurring subscription revenue is highly predictable: once a customer is paying, the default assumption is that they continue paying. This predictability reduces the risk buyers absorb when acquiring the business.

In the lower middle market (sub-$5M ARR), SaaS businesses typically trade at 3x to 6x ARR. High-growth SaaS with strong net revenue retention (NRR above 110%) and low churn can push toward 6x to 8x or higher. At the institutional level, where strategic acquirers and PE-backed rollup platforms compete, multiples compress slightly as deal structures get more complex, but best-in-class assets still command premium pricing.

What buyers are paying for in SaaS:

- Monthly or annual subscriptions that create a predictable revenue floor

- Net revenue retention above 100%, meaning revenue grows from the existing customer base without new sales

- Low variable costs once the product is built (gross margins of 70% to 85% are standard)

- Software infrastructure that is not tied to a specific founder’s technical involvement

- Customer contracts or annual commitments that create switching costs

The multiple applied to ARR is really a function of how confident the buyer is that the revenue will persist after the acquisition. High churn SaaS (above 5% monthly) trades at discounted multiples for the same reason a DTC brand with poor retention trades at a discount: the revenue is not durable.

How Ecommerce Multiples Work

Ecommerce businesses are valued primarily on a multiple applied to seller’s discretionary earnings (SDE). SDE is the business’s net profit after adding back the owner’s compensation, one-time expenses, and non-cash charges. For larger ecommerce businesses (typically above $2M SDE), buyers may shift to EBITDA as the earnings base, which excludes addbacks for owner compensation and applies a similar multiple logic.

In the lower middle market, DTC and Shopify businesses trade at 2.5x to 5x SDE. Amazon FBA businesses in the same range trade at similar multiples, though aggregator-driven demand compressed to the 2.5x to 3.5x range from its 2021 peak. Multi-channel businesses with both Amazon and Shopify presence can attract premiums at the higher end of those ranges.

What buyers are paying for in ecommerce:

- Trailing 12-month SDE as the earnings baseline

- Revenue quality: repeat purchase rate, LTV, and cohort retention

- Brand defensibility: trademarks, customer awareness, and organic demand

- Operational independence: how much of the business runs without the founder

- Channel diversification across paid, email, organic, and direct

The multiple is applied to a profit figure, not a revenue figure, which means gross margin matters enormously in the ecommerce valuation. A business with 60% gross margins and $500K SDE will attract different buyer interest than one with 35% gross margins and the same SDE figure. For a detailed breakdown of every driver that moves an ecommerce multiple up or down, see our guide to DTC Brand Valuation: The 7 Factors That Move Your Multiple.

The Core Reasons SaaS Multiples Exceed Ecommerce Multiples

The gap between SaaS and ecommerce multiples is real and persistent. It is not a market inefficiency buyers have failed to correct. It reflects structural differences in these two types of businesses that create genuinely different risk profiles.

Revenue predictability is the single largest driver. A SaaS business with 1,000 monthly subscribers at $99/month enters every month with a revenue floor of roughly $99,000. An ecommerce brand with the same monthly revenue has to earn that revenue again from customer acquisition, repeat purchases, and conversion. The SaaS model creates contractual revenue; the ecommerce model creates transactional revenue. Buyers pay a premium for predictability.

Gross margin is the second major driver. SaaS gross margins of 70% to 85% are achievable because the marginal cost of delivering software to one more customer is effectively zero. Ecommerce gross margins of 35% to 55% are constrained by physical cost of goods, fulfillment, and returns. A $1 million revenue SaaS business at 75% gross margins generates $750K in gross profit. A $1 million revenue DTC brand at 45% gross margins generates $450K. The gap in absolute profit compounds the multiple gap.

Operational scalability is the third driver. A SaaS product scales without proportional cost increases: the engineering team, infrastructure, and support costs grow more slowly than revenue. Ecommerce scaling requires proportional increases in inventory, fulfillment capacity, customer service, and often ad spend. Buyers model future cash flows, and the SaaS model’s scaling economics create more optimistic projections.

The most common ecommerce valuation misconception: founders who see a competitor SaaS business sell for 6x revenue and expect their ecommerce brand to trade at a similar revenue multiple. Ecommerce multiples are applied to profit (SDE), not revenue. A DTC brand doing $2 million in revenue with $400K SDE at 4x sells for $1.6 million, not $8 million.

Where Ecommerce Multiples Close the Gap

The structural gap between SaaS and ecommerce multiples is real, but it is not fixed. Specific ecommerce business types and characteristics consistently command multiples that narrow or close the gap with comparable SaaS businesses.

Subscription and replenishment-based DTC brands are the clearest example. A brand that sells consumable products (supplements, skincare, coffee, pet food) on subscription generates predictable recurring revenue that buyers value similarly to SaaS. A supplement brand with 60% of revenue on active subscriptions, a 12-month retention rate above 40%, and a 3.5x LTV:CAC ratio is valued on fundamentally different logic than a brand that relies entirely on one-time transactional purchases. These businesses regularly achieve 4x to 6x SDE multiples from buyers who specifically target subscription-driven brands.

High-repeat, brand-loyal businesses in niche categories also compress the gap. A premium outdoor gear brand with 45% repeat purchase rates, strong organic brand search volume, and a defensible audience (email list of 80,000 engaged subscribers) is not valued the same way as a generic dropshipping business. Brand loyalty and organic demand function as recurring-revenue proxies because they reduce customer acquisition cost and increase revenue predictability.

Proprietary products with IP protection matter more than most founders expect. A business with registered trademarks, patent-protected formulations or designs, and exclusive manufacturer agreements is structurally more defensible than one operating on easily replicated white-label products. IP creates switching costs for buyers and barriers to competition that support higher multiples.

What buyers in each segment examine:

- Subscription businesses: monthly recurring revenue, churn rate, average subscription lifetime, cohort LTV

- Brand-loyal businesses: repeat purchase rate, brand search volume, email engagement rates, organic traffic share

- IP-protected businesses: trademark registration status, patent filings, exclusivity agreements with manufacturers

For additional detail on how revenue quality affects your ecommerce multiple, see Ecommerce Multiples in 2026: Real Deal Data from EcomSwap.

Deal Structure Differences Between SaaS and Ecommerce Acquisitions

Beyond the headline multiple, SaaS and ecommerce deals are often structured differently in ways that affect the total consideration a seller receives and the conditions attached to the payment.

SaaS deals are more frequently structured with a higher proportion of upfront cash because the recurring revenue model makes forward-looking projections more reliable. If a SaaS business has $500K ARR and 5% annual churn, a buyer can model Year 2 revenue with reasonable confidence. That confidence supports higher upfront payment because the risk of revenue shortfall is lower.

Ecommerce deals more commonly include earnouts or seller notes, particularly for businesses above $2M SDE. An earnout ties a portion of the purchase price to the business hitting revenue or profit targets in the 12 to 24 months post-close. For the seller, this creates upside if the business grows. For the buyer, it reduces the risk of overpaying for a business whose near-term trajectory was overstated. The proportion of deal price that comes in deferred consideration is generally higher for ecommerce than for comparably sized SaaS businesses.

Transition periods also differ. SaaS acquirers often need a shorter transition because the product and infrastructure operate independently of the founder once documentation is in order. Ecommerce transitions are typically longer (60 to 90 days) because supplier relationships, operational knowledge, and brand voice are more founder-dependent. A shorter, cleaner transition is achievable with thorough SOP documentation and a well-prepared data room, and it consistently supports better deal terms.

The most common deal structure issue in ecommerce exits: sellers who accept earnout structures without fully modeling the operational commitments required to achieve them. An earnout that pays out $500K contingent on maintaining 15% year-over-year growth for two years post-close is only valuable if the seller either remains involved or the buyer has the team to drive that growth. Model the earnout scenario conservatively before accepting it as part of your consideration.

What Ecommerce Sellers Can Do to Improve Their Multiple

Understanding the gap between SaaS and ecommerce multiples is useful. But for founders actively preparing for an exit, the more practical question is: what levers move an ecommerce multiple upward, and how much lead time is required to pull them?

The highest-leverage improvements for ecommerce multiples are not financial engineering. They are operational and revenue-quality improvements that change the risk profile buyers assign to the business.

What to prioritize in the 12 to 18 months before going to market:

- Build subscription or replenishment revenue. Even 20% to 30% of revenue on subscription meaningfully improves buyer perception of revenue predictability. Introduce a subscription option on your top-selling replenishable SKUs and track subscriber retention monthly.

- Reduce channel concentration in paid social. A business that acquires 80% of customers through Meta ads is one algorithm change or cost increase from a compressed margin. Building email, organic SEO, and direct channels diversifies the revenue base and reduces perceived risk.

- Document your operations. SOPs for supplier communication, fulfillment management, customer service, and paid media management tell buyers the business runs without you. Every hour you spend on documentation before going to market pays off in multiple protection at close.

- Protect your IP. If your brand trademark is not registered, file it now. The USPTO process takes 8 to 12 months and a registered mark is a concrete asset that appears in every buyer’s IP review.

- Clean your financials. Two years of bookkeeper-prepared, accrual-basis P&Ls that reconcile to bank statements reduce the uncertainty discount buyers apply during review.

The businesses that close the gap with SaaS multiples are not the ones with the highest revenue. They are the ones that have deliberately built characteristics that reduce the risk premium buyers apply: predictable revenue, documented operations, diversified channels, and protected IP.

How to Choose Between SaaS and Ecommerce Acquisitions as a Buyer

For buyers and investors evaluating both asset classes, the choice between acquiring a SaaS business and an ecommerce business is not simply a matter of which multiple looks better. It reflects a view on operating competency, risk tolerance, and growth thesis.

SaaS acquisitions suit buyers with technical or product backgrounds who can evaluate software infrastructure, understand retention economics, and manage or hire engineering capacity. The risk in SaaS acquisitions is often product risk: will the software remain competitive, and does the product roadmap require ongoing technical investment? Buyers without technical depth frequently overpay for SaaS businesses by underweighting the ongoing development cost required to maintain competitive positioning.

Ecommerce acquisitions suit buyers with operational, marketing, or supply chain backgrounds. The key risks in ecommerce acquisitions are supplier concentration, channel dependency, and inventory management. A buyer who understands paid social, can optimize a Klaviyo flow, and has experience managing a 3PL has a genuine operational advantage in ecommerce assets that a purely financial acquirer does not.

What experienced acquirers examine before committing:

- Total cost of ownership beyond the purchase price (development costs for SaaS, inventory and COGS for ecommerce)

- Operational complexity relative to team capacity

- Growth thesis: is the plan to optimize the existing business, expand distribution, or use the acquisition as a platform for add-ons?

- Exit path: what is the likely buyer profile in 3 to 5 years, and does the asset class fit that profile?

The buyers who generate the best returns in ecommerce acquisitions are not passive holders. They are operators who have a specific thesis for improving repeat purchase rates, expanding to new channels, or introducing subscription mechanisms that improve the business’s revenue profile and, ultimately, its resale value.

Bottom Line

SaaS businesses trade at higher multiples than ecommerce businesses for structural reasons that reflect real differences in revenue predictability, margin profiles, and operational scalability. A SaaS business at 4x to 6x ARR and an ecommerce brand at 3x to 4.5x SDE are both rationally priced assets when you understand what each multiple is compensating the buyer for.

For ecommerce founders, the gap is not insurmountable. Subscription revenue, documented operations, diversified channels, and protected IP are the four levers that consistently move ecommerce multiples toward the upper end of the range and, in some cases, toward SaaS-like territory for the most well-built DTC brands. The best time to start pulling those levers is not six months before you go to market. It is now.

If you are evaluating where your ecommerce business stands today and what realistic exit value looks like, EcomSwap offers free valuations for qualified DTC, Shopify, and Amazon FBA businesses. Our team works with founders at every stage of exit preparation, from early-stage clean-up to active listing and deal negotiation.